Axios Nails It; Is IR Finally Catching Up & Going Digital?

A few weeks ago, a colleague flagged for me a pleasantly surprising article in Axios about companies modernizing the way they distribute earnings information. Eleanor Hawkins’ reporting describes an emerging trend towards what Sinter would call more digital and social IR. I write “pleasantly surprising” because, for the most part, the average public company still does very little with its IR web presence, and looks at digital and social channels mostly as afterthoughts. This mindset is something that small- to mid-cap companies in particular should change.

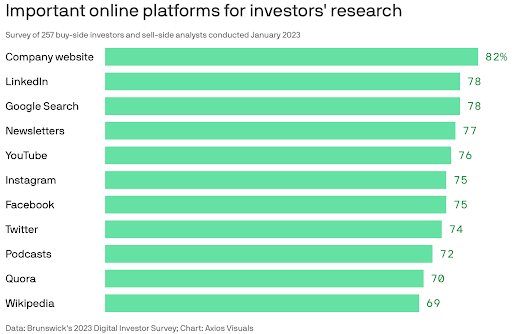

The hook for Axios piece appears to be a 2023 survey by the fine people at Brunswick Group that documents the significant importance of digital and social channels for investor information uptake and gathering. This was a telling graphic:

Axios, armed with the survey, did its usual high-quality and click-worthy reporting. The piece cited high-valuation, newsworthy, cool-kid tech companies like Spotify, Netflix, and AirBnB, as well as Dorsey-era Twitter, as examples of public businesses doing something more modern with their earnings process.

We couldn’t applaud both Axios and these companies more for breaking out of the 1970’s-style approach to IR on which most listed companies still depend - e.g, exchanging information with the capital markets only through 4x/year earnings press releases; powerpoint decks; audio calls disguised as webcasts; and occasional investor days and conference appearances.

It’s not so much that companies have to stop doing these types of classic investor disclosure. It’s more that the impact of the classics has declined pretty precipitously in the last 15-20 years in terms of how the markets, investors and analysts acquire information and make decisions about public equities.

This is particularly the case for companies that are not, organically, in headlines every day like the ones cited by Axios. Not every company, after all, is Spotify. Its stock is performing extremely well - up over 75% YTD, way ahead of major indexes. It doesn’t necessarily need more analyst coverage (it has 20-plus sells-side followers), has its own entry in Investopedia about how it makes money, is 90% held by insiders and institutions, and enjoys mega-cap status.

In other words, it probably could just upload filings to the SEC’s EDGAR database and call it a day, from a shareholder engagement perspective. However, as the article points out, Spotify clearly believes it’s worth making its performance more accessible, understandable and engaging to the markets via a non-standard approach to IR.

Why don’t more companies do this - especially the thousands of publicly-listed businesses that don’t enjoy Spotify’s size, scale and performance advantages?

The basic premise that more accessible and relevant online information drives investment decisions, and that digital and social discoverability can mediate these decisions, isn’t really arguable at this point.

If you don’t want to take ours Brunswick’s, or Axios’ word for it, there’s plenty of detailed, quantitative, peer-reviewed academic research supporting this truth.

Basically, even if a company doesn't offer investors new, material information, but still makes the information that IS available easier for shareholders to get, and refinforces and explains that information in real time, with relevant context?

On average, over time, that company’s stock will correlate with higher valuations and better stock price performance.

For the Spotify’s of this world, this is relevant but not critical - because of the size and scale of its business and the investment it has made for years in marketing that business as well as its streaming product.

For the thousands of smaller, less visible public companies out there, however, this reality IS critical. But it often remains overlooked by CFO’s, CEO’s, IR folks and Boards.

So it was great to see Axios highlighting a few examples of strong companies taking an innovative, even disruptive approach to IR. More pointedly, it was refreshing to see an approach to capital markets interaction that aligned with the same kinds of principles, tools and behavior that these innovative companies use to sell their products and services.

Too many public companies confuse disclosure with marketing, and business performance with business models. Shareholders and trading software know the difference, however. So, quite often - and regardless of their performance - companies that ignore more digital and social approaches to IR operate at a disadvantage with respect to the capital markets and their competition.

The good news? These days, it’s more possible than it has ever been for any company to adjust, catch up, and take more agency over valuation.

# # #