How Smart Companies See Investor Relations/IR

In our prior blog post, we described the drawbacks of confusing business performance with business models. We also outlined the limitations of traditional investor relations, vs. what we call value marketing.

Even companies that have been public for a long time don’t spend a lot of time thinking deeply about investor relations. Yet, when one takes a closer look at what IR really should be - i.e., a corporate function focused on building and protecting capital markets value - overlooked opportunities emerge that can benefit any public company, as well as many private ones.

Management teams, Boards and employees (as well as investors and analysts) do pay attention to stock prices, of course. But for decades, it’s been an IR truism that there are too many factors influencing equity pricing for the investor function/a company to be fully responsible for stock prices at any given moment in time.

The accepted wisdom: if you operate the company well, results follow. And with good results, comes a high multiple. The opposite also presumably holds true.

We wouldn’t argue that a company can’t control its stock price except at the edges. Nor would we question that poor operations, execution and results equate to low multiples.

But we also know that the hoary truism above hides a multitude of sins, so to speak - including companies avoiding any accountability whatsoever for valuation (“it’s just the market”); insisting that performance is the only thing that matters to stock price; defaulting only to traditional IR because it’s “low risk,” or “what the market understands,” etc.

Faced with the dilemma of how to make investment narratives and performance impactful, it often helps our clients to take a beat and consider IR more fundamentally.

The Four Key Elements of IR

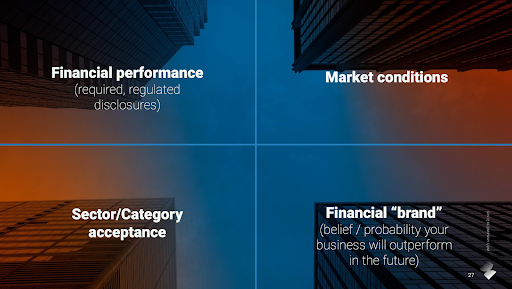

While there are many descriptions of investor relations, we prefer to break it down into four areas (see also figure 1):

Financial performance - or regulated, required disclosures of company results, e.g., 10Qs, annual reports, proxy statements, etc.

Market conditions - i.e., trends, patterns, headwinds and tailwinds including information, sentiment or events that move equities regardless of how a company, or even a sector, might actually be performing. Examples include the supply chain issues during the pandemic; the breakout of major regional conflicts; significant elections, interest rates, etc.

Sector/category acceptance - if market conditions are the bigger-picture context, sector/category acceptance is what we call a more localized context for a given company stock. What KIND of company is it/where does it fit? How obviously does it really fit into an industry vertical, like autos, or insurance, or consumer tech? Do the sector and various peers define your company, or does the company define the sector?

“Financial brand,” or the belief (among humans) and the probability (for algorithms driving trading software) that a company has the qualities and capability to outperform in the future.

Figure 1

The standard view of the relative importance of these elements and their impact on stock price looks something like Figure 2. That is, it’s assumed that financial performance and market conditions represent the biggest part of the IR function and its impact on a stock.

Figure 2

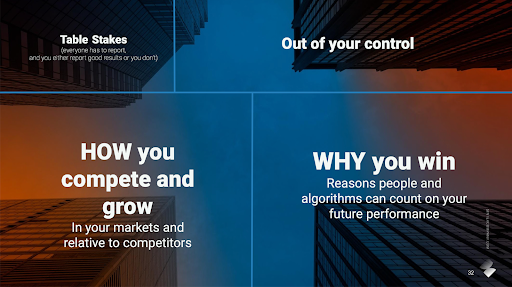

Smart companies with generally higher valuations - whether larger-cap or not - don’t see it this way. They understand that, in fact, good IR looks more like Figure 3. They know, in other words, that the most powerful levers they have for building/protecting market value lie in the areas of sector acceptance and financial branding.

Figure 3

Substituting some terms, it’s easy to see why this is the case, in Figure 4.

Figure 4

When you truly think about it, results are table stakes. You have to report and package them in specific ways, like GAAP accounting - and the results are what they are, good or bad. Meanwhile, market conditions, though relevant, are fully out of any one business’s control - even a mega-cap. As an aside, this is of course why market conditions so frequently are used as excuses by companies for weaker-than-expected results, whether or not that’s actually true.

Smart, high-multiple companies see it differently. For them, instead, the areas of maximum influence for a company with respect to equity performance are - in contrast to standard assumptions - better, more frequent explanation of how that business will compete and win, in its markets, vs. competors; and why that success is more, rather than less, likely in the future.

The challenge most companies, especially smaller-cap companies, have with the capital markets isn’t lack of information. It’s the lack of frequent, contextualized visibility.

Public companies are required to disclose their results - and most of them do just that, and little more. What they should do, in addition, is market their markets and continuously re-explain their business models, in real-time, with reference to relevant events and unique insights.

If the context for a business’ performance is widely accepted? Then that performance will be better appreciated by the markets when it is good, and less disruptive when results are weaker.

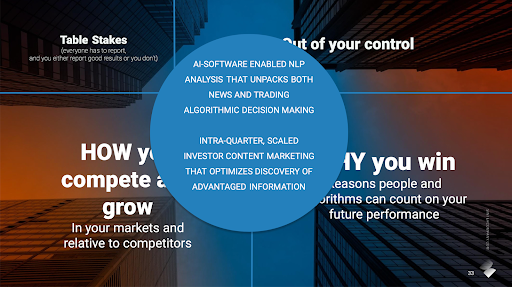

The four part framework above is helpful on its own for companies to re-think how they can leverage their financial information and better self-advocate. However, for it to be truly practical, it must be translated into a programmatic, tactical campaign-style approach to supporting a higher multiple - using a combination of digital content and AI-informed analytics (Figure 5).

In subsequent posts, we’ll talk more about how and why to develop this kind of IR function and capabilities.

Figure 5

# # #