The ABC’s of MARKETING YOUR MARKET, vs. Just Citing a TAM

In a recent post we wrote about the utility of economic fame and the importance of business model discoverability for private and public companies. This post zeroes in on a key principle of our approach to competitive economics: properly marketing a tightly-defined market, vs. just serving business audiences a TAM (total addressable market) figure with a side of CAGR.

We explained elsewhere that financial performance amounts to table stakes when it comes to high-quality, high-impact investor marketing. A company’s results over a given time period are what they are. You can’t change those numbers much. (If you think you can, we probably aren’t working with you on investor positioning, but you might be/become a crisis client).

Don’t misunderstand: financial results matter in the sense that up-and-to-the-right is better than flat, or down. But as smart companies know, the larger context for results can influence valuations and multiples almost as much as performance, especially over longer timescales.

A key part of this kind of influential context: thoughtful, unique market definitions - emphasis on “thoughtful,” “unique” and “definition.”

Do This

A good market definition explains a business’s assumptions about and plans for a defensible economic opportunity, vs. just estimating portions of a growing spend.

It doesn’t just feature big, dumb numbers (see below). It tells a story about an overlooked commercial opportunity specific to a company that aligns with an equally specific business model.

While companies should tailor this story very carefully for it to be effective in making a positive difference to valuations, some general features of a strong market definition include:

A: Framing a market in terms of a problem tied to an unmet customer need or want.

Problem statements are a big part of private-company fundraising, though often they are too fuzzy or exaggerated (we’ll return to this in another post).

However, most public companies leave them behind, except in a brand/product context, to the detriment of multiples and shareholders. The assumptions seems to be that if a company is public, it’s market and customer-product fit is so well understood that it’s already baked into the stock price.

In our experience, while assumptions about the future revenue/profit opportunities for public companies definitely are reflected in the stock price, much of the time those assumptions don’t align with management’s own views or operating strategy.

In part, this is because many companies overlook market definitions as a key lever in providing context for both results and for guidance.

B: Identifying “stackable” revenue drivers within a given market definition.

With this kind of problem set-up, the next useful part of any good market definition aligns with convention. That is, both public and private companies should take the time to define and maintain a TAM/SAM/SOM fact pattern.

(That’s TAM, or total addressable market/the broadest credible projected revenue opportunity for a company; SAM, a smaller serviceable addressable market, bounded by core competencies; and SOM, a still-narrower serviceable obtainable market estimating revenues from shorter-term marketshare targets.)

Many companies, especially public ones, just offer a TAM - and make it as big and high-growth as possible. This is risky/unproductive, in that it can set expectations too high and render company FP&A less credible when/if the business doesn’t perform well enough. For this reason, the effort to outline some version of SAM/SOM can be quite useful.

These three datapoints, however, don’t themselves form a compelling market narrative. Here, any company has the opportunity to make its economic-opportunity story more specific. For example:

Does it have insights into a very particular buyer or market segment that competitors might not (military-use specs and certifications)?

Is there something objectively distinct about its products (Nvidia chips, for now)?

Are there tax incentives for making, buying or using its products (EV’s)?

Is there a larger, secular trend in culture/business/markets that gives it a tailwind superior to other offerings (growth of home offices)?

The bullets above are examples of what Sinter calls stackable revenue drivers, or factors that make a business’s revenue opportunity more probable for algorithms and more credible for people.

Put another way, citing market size and market growth alone is somewhat like claiming, of a product, “our XX tastes good.” That’s a limited claim.

Better to explain, e.g., why taste matters in your sector; why your investments in taste produce superior purchasing trends; and/or that younger generations are increasingly seeking a particular kind of taste that only you provide.

This kind of market narrative, combined with a good problem statement and TAM/SAM/SOM variations comprise a strong market definition - i.e., one framed in terms of intuitive demand drivers and competitive moats.

C: Amplify and sell in the revenue opportunity story - i.e., market it like a product.

Many companies, especially public ones, do flag for investors and others some of the datapoints, facts and types of claims referenced above.

But usually, this information is scattered across and/or buried in quarterly filings, earnings call transcripts, investor decks and on the product portions of websites.

It’s not consolidated, curated and marketed in an ongoing campaign that trains investors and investing software in how best to interpret your performance. In other words, most companies don’t use market information as a unique advantage in the face of competitors, events and other trends.

With relatively minor effort, however, It can and should be. Shareholder letters, IR site homepages, investor decks, 10Q MD&A business overview sections, and earnings collateral all can routinely reference a defined, long-term market opportunity as context for shorter-term performance. This work correlates with higher multiples.

This is what we mean by “marketing your market.”

A Hypothetical Example in an Out-of-Favor Sector

E.g., suppose you manufacture commercial EVs, maybe the short-haul FedEx trucks that deliver packages to homes and businesses. A good market definition for this business does not just jump right to regurgitating EV market size and projected growth.

Instead, “EVCO” might anchor its market in the problem of fleet-owner TCO, or total cost of ownership. Why? Because this defensibly is the core problem the company solves.

Growing demand for deliveries = more packages = more trips by more trucks = more wear-and-tear = more fleet-owner costs.

Suppose EVCO has data showing that its vehicles have lower TCO than diesel-powered ones? Suddenly its economic opportunity becomes more compelling.

EVCO isn’t just selling electric trucks into a crowded EV market. It’s solving a major fleet-operator problem, and increasing profits/lowering costs for huge companies with each truck it sells.

Also: the more trucks it sells, the bigger the TCO impact - which sets up an EVCO claim about network effects, a dynamic that can help drive a high multiple.

Note: just citing lower-than-diesel TCO as a feature of its vehicles undersells EVCO, itself. Lower per-vehicle TCO is a product marketing tactic, not an investor-marketing strategy.

Any TAM/SAM/SOM that EVCO shares, in this example, would now would have insightful context, vs. just duplicating industry projections shared by dozens of other companies making EVs.

Following Sinter’s “A-B-C” approach to marketing its market, EVCO also has the option of describing multiple layers to its revenue opportunity.

It can claim a product-defined economic opportunity (it sells electric trucks at a given price).

It can cite logistics/package delivery growth as an accelerant to demand for its particular EVs, given a TCO advantage.

It can also define its market and its revenue opportunity in terms of federal, state and local tax incentives for electric trucks.

It can cite state regulations requiring fleets to lower emissions.

Maybe it can also highlight more manufacturing capacity or customers than competitors.

This kind economic narrative goes beyond TAM/SAM/SOM, and makes the revenue opportunity highly specific to the company, in terms that advantage its business.

What Not To Do

For those who enjoy or are aided by negative examples, vs. just counsel? Read on.

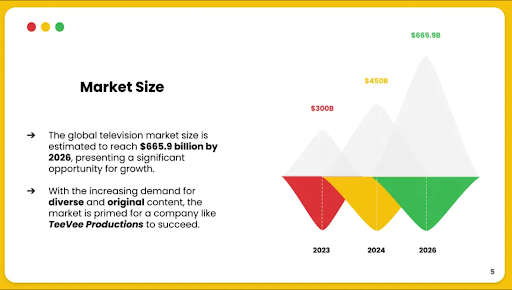

We do a lot of fundraising work with earlier-stage private companies, so we’ve seen and built a great many pitch decks. For better and often worse, pitch convention calls for a “TAM slide.” As many VCs and pitch advisors note, however, these slides can lack substance and/or be genuinely terrible visuals by Tufte standards (e.g., Figure 1).

Figure 1

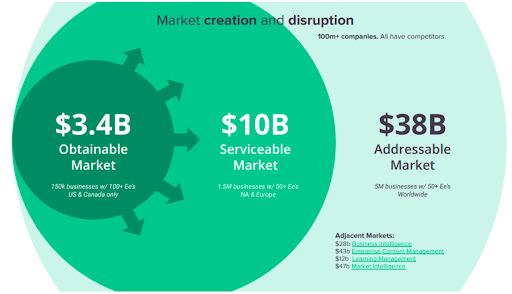

Even versions of this kind of slide with better visual and information design tend to share the same drawbacks. They look numbingly similar; they focus attention on big-but-dumb numbers; and they fail to show conviction about a distinctive economic opportunity (Figure 2).

Figure 2

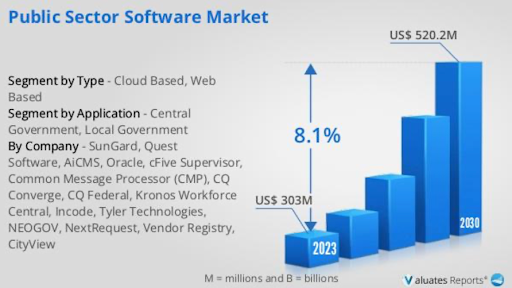

Public-company investor decks generally suffer from similar issues. They often leave out the SAM/SOM (in fairness, so do plenty of private startups), and showcase increasingly big, dumb numbers (Figure 3).

Figure 3

TAM Thirst

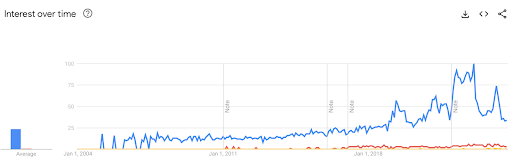

And regardless of the availability of counsel to approach the topic differently, the obsession with TAM shows no real signs of slowing down - as a graph of search activity in the US comparing TAM (blue) with SAM and SOM (red and yellow, respectively) over the past 20 years illustrates (Figure 4). The worldwide search results graph over the same time is even more extreme.

Figure 4

Big dumb numbers as we noted above don’t provide useful economic or strategic context for investors, whether private or public. Shareholders and potential shareholders want to know about a specific and defensible revenue opportunity.

If a market is large, accepted and established, you don’t need to promote how large and established it is. In fact, doing so might undermine investor conviction if your business is subscale - because you’ll immediately raise questions about your ability to compete.

If a market is niche or emerging or both? You need the kind of informed economic narrative we outlined further above. And in fact, if you are competing in a large and established market, you need to make it MORE niche, so that you give investors a credible reason to believe you can capture a competitive share of the opportunity.

All of this is to some extent easier said than done. However, it’s also true that any company can define and share a more compelling market definition explanation. And given the way both algorithms and people discover information and make decisions today, doing so is one of the strongest levers any business has for improving the impact of its performance.